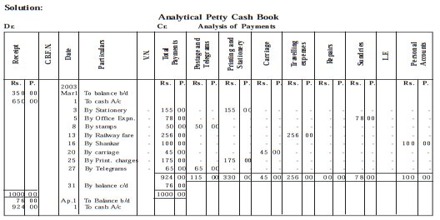

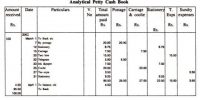

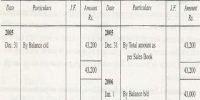

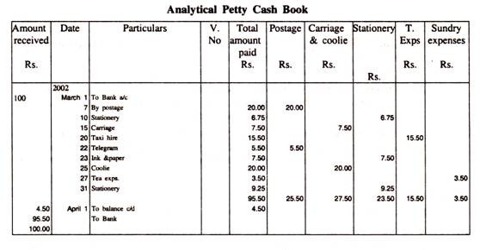

Balancing Petty Cash Book

At the end of the period i.e., week or month the whole payments column and individual expenses columns are totaled. It should be ascertained that the whole of petty expenses column must be equal to the total of payments column. The total payments column is compared with the whole of receipts column and balance is obtained. The closing balances are shown as ‘By Balance c/d’. The closing balance is carried forward to the beginning of the next week or month. It is shown as ‘To Balance b/d’.

Illustration: A Petty cash book is kept on Imprest system, the amount of imprest being Rs.1,000 and has seven analysis columns for Postage and Telegrams, Printing and Stationery, Travelling Expenses, Repairs, Carriage, Sundry Expenses and Personal Accounts. Enter the following transactions:

2003 March 1. Petty cash in hand Rs.350

Date: 1. Received cash to framework imprest Rs.650

3. Paid for stationery Rs.155

5.Paid office expenses Rs. 78

8.Bought stamps Rs. 50

13.Paid for transtort fare Rs.256

16.Paid to Mr. ABC Rs. 100

20.Paid for carriage Rs.45

25.Paid for printing charges Rs. 175

27.Paid for telegram Rs. 65