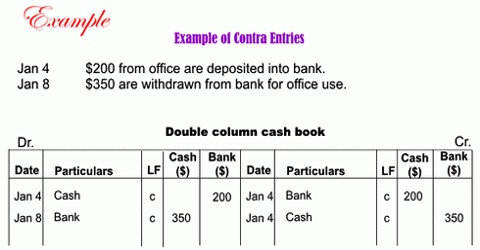

Contra Entry

Contra entry is an adjustment entry between banker and customer. When an entry affects both cash and bank accounts it is called a contra entry. Contra in Latin means the opposite. In contra entries, both the debit and credit aspects of a transaction are recorded in the cash book itself. This account is a general ledger account which is intended to have its balance be the opposite of the normal balance for that account classification.

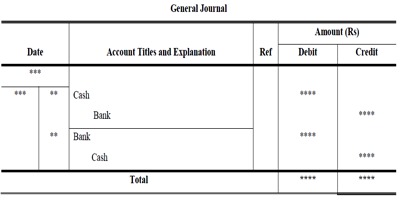

Example: Cash paid into bank

Bank A/c Dr. x x x

To Cash A/c x x x

(Cash paid into bank)

This is a contra entry. As the cash book with cash and bank columns is a joint cash and bank account, both the aspects of the transaction will be entered in the similar book. In the debit side ‘To Cash A/c’ will be entered in the details column and the amount will be entered in the bank column. In the credit side ‘By Bank A/c’ will be entered in the particulars column and the amount will be entered in the cash column.

Such contra entries are denoted by writing the letter ‘C’ in the L.F. column, on both sides of the cash book. They designate that no posting in reverence thereof is essential in the ledger.