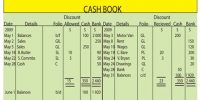

A cash book is an exceptional journal which is used to record all cash receipts and cash payments. Cash book is written by depositor and pass book is written by the bank. All transactions related to a bank are recorded in the bank column of the cash book and these transactions are also recorded in the pass book by the bank.

Difference between Cash Book and Pass Book –

Cash Book – A book that keeps a record of cash transactions is known as cash book.

- Cash book keeps a record of cash transactions. It is written by the depositor.

- Money deposited is recorded on the debit side and money was withdrawn on the credit side.

- Debit balance shows cash at the bank while the credit balance shows overdraft.

- A check deposited for collection is recorded on the date of deposit.

- A check when issued to a creditor is recorded on the date of issue.

- It’s debit balance shows cash at bank and credit balance shows bank overdraft.

- Cash book is where receipt or payment of money is recorded. In this case, it is not issued by the bank but can be used to keep track of transactions within the bank account.

Pass Book – A book issued by the bank to the account holder that records the deposits and withdrawals is known as Pass book.

- Passbook is issued by the bank to the account holder that records the deposits and withdrawals. It is written by the bank but remains in the depositor’s possession.

- Money deposited is entered on the credit side and withdrawn on the debit side.

- Debit balance shows overdraft while the credit balance shows cash at bank.

- It is recorded on the date when it is actually collected from the debtor’s bank.

- It is recorded when it is paid by the bank to the creditor.

- It’s debit balance shows bank overdraft and credit balance shows cash at the bank.

- Pass Book is particularly issued by a bank for its account holders to record deposits & withdrawals in a specific Bank Account.

The key difference is:

Cash book refers to a business journal in which all the cash transactions of the business are recorded in a sequential manner. The debit side shows cash receipts and the credit side shows cash payments. The record is helpful in the preparation of the ledger. It is a subsidiary book. All cash and cheques received and deposited are shown on the receipt side. All payments made by cash and cheques are shown on the payment side. At the end of a given period, its balance is obtained to know the amount of cash and bank balances.

Pass book is a book that records the bank transactions in a savings account. It is a summarized statement of all deposits and withdrawals made by the depositor during a certain period of time. It is the exact copy of the customer’s account in the bank’s book. It records the deposits, withdrawals, interest credited, bank charges, etc. during a financial year. The passbook shows the balance of the client after each deposit and withdrawal. It has two sides i.e. debit side and credit side.