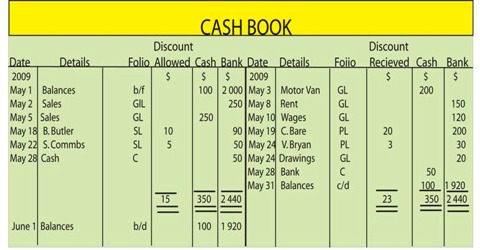

Debit Side and Credit Side of the Cash Book

All transactions in the cash book have two sides: debt and credit. All cash receipts are recorded on the left hand side, and all cash payments are recorded by date on the right hand side.

On the debit side of the cash book, the bank column represents:

(i) Cheques deposited into bank for collection.

(ii) Cash paid into bank and

(iii) Some entries that are made only after receiving the information from the bank viz.,

- Amounts collected by the bank on our behalf as per the standing instructions, for example, Interest collected on investment.

- Interest given by the banker for the balance kept by us in our bank account.

- The amount paid by our customers directly into our bank account.

On the other hand, on the credit side of the cash book, represents:

(i) Cheques issued for payment.

(ii) Cash withdrawn from bank for office use and personal use.

(iii) In addition, some entries are made after receiving information from the bank viz.,

- Amounts paid by the bank on our behalf as per the standing instructions, for example, payment of insurance premium.

- Interest charged by the bank for the amount drawn over and above the actual balance kept in the bank account.

- Bank charges payable for the agency and utility services rendered by the bank.