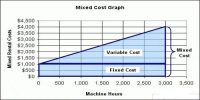

Fixed Costs create difficulties in Costing Units of products

Fixed costs can create difficulties if it becomes necessary to express the costs on a per unit basis. Total cost does not change with changes in the volume of activity (within a relevant range). The cost per unit will change as the number of units change. Rent, insurance, administrative salaries are examples of fixed costs. These costs do not change just because you make or sell one more unit as long as you stay within the relevant range. Some examples of fixed costs include rent, insurance premiums, or loan payments. Fixed costs can create economies of scale, which are reductions in per-unit costs through an increase in production volume. This idea is also referred to as diminishing marginal cost.

Average fixed cost per unit is dependent on the number of units manufactured. As production increases, the cost per unit falls as the fixed cost is spread over more units. On the other hand, as production declines, the cost per unit increases since the fixed cost is spread over fewer units. This is because if fixed costs are expressed on a per unit basis, they will react inversely to changes in activity. In the hospital, for example, the average cost per test will fall as the number of tests performed increases. This is because the £8,000 rental cost will be spread over more tests. Conversely, as the number of tests performed in the clinic declines, the average cost per test will rise as the £8,000 rental cost is spread over fewer tests.