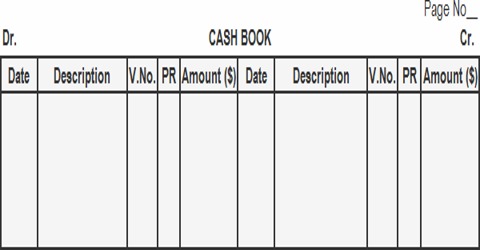

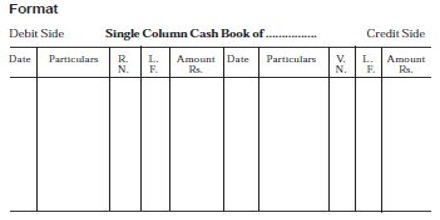

Format of Single Column Cash Book

Single column cash book (simple cash book) has one amount column on each side. It is a cash book that is used to record only cash transactions of a business. The single-column cash book look likes a T shaped cash account in approximately all compliments. The pages of this book are perpendicularly divided into two equal parts. Only cash transactions are recorded in this book. All cash receipts and payments are recorded systematically in this book. The receipts being entered on the left (debit) side and payments on the right (credit) side. It has simply one money column on debit and credit sides to record cash transactions, which is why it is called a single column cash book.

The purpose of columns used on both sides of a single column cash book is briefly explained below:

- Date:

The date column of the cash book is used to record the year, month, and actual date of each cash transaction. This column shows both the debit and credit side. It proceedings the date of receiving cash at the debit side and paying cash at the credit side. There is no need to repeat year and month for the additional entries until a new month starts or a new page is needed.

- Particulars:

This column is used at both the debit and credit side. This column is used to record the account titles to be debited or credited as a result of each cash transaction. It records the names of parties (personal account), heads (nominal account), and items (real account) from whom payment has been received and to whom payment has been made. After recording the opening balance in the particular column, the cash transactions of the current period are recorded.

- Receipt Number (R.N):

This refers to the serial number of the cash receipt. This column is used to write the page number of each ledger account named in the description column of the cash book. The serial number of the debit vouchers is recorded on the debit side and the serial number of credit vouchers is recorded on the credit side in the voucher number (V. No.) column of the cash book.

- Voucher Number (V.N):

A voucher is a document that supports a business transaction. This refers to the serial number of the voucher for which payment is made. This column is used to record the serial number of a receipt voucher or payment voucher. When money is received, a receipt in original is given to the payer and a copy of it is retained by the payee.

- Ledger Folio (L.F):

This column is used in both the debit and credit side of the cash book. The ledger page (folio) of every account in the cash book is recorded against it. When entries from cash book are posted to ledger accounts, the relevant account number is written in this column.

- Amount:

This column appears on both sides of the cash book. The amount column is used to enter the amount received or paid as a result of a cash transaction. The amount column of a single column cash book is used to record the money value of each cash transaction. The actual amount of cash receipt is recorded on the debit side. The actual payments are entered on the credit side.