Meaning of Accounting Cycle

An accounting cycle is an absolute chain of accounting procedure, which begins with the recording of business transactions and ends with the preparation of final accounts. The accounting cycle is usually started and finished transversely an accounting period, generally a financial part or a fiscal year.

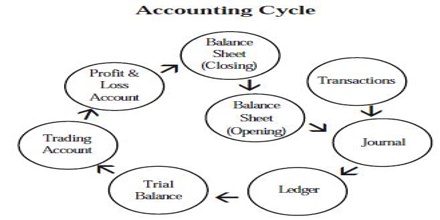

When a businessman starts his business activities, he records the day-to-day transactions in the Journal. From the journal, the transactions move further to the ledger where accounts are written up. Here, the combined effect of debit and credit pertaining to each account is arrived at in the form of balances.

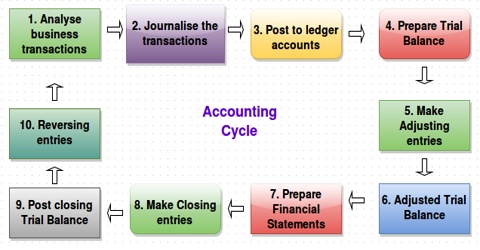

The accounting cycle is regularly described as a procedure that includes the following steps: identifying, collecting and analyzing transactions, recording the transactions in journals, posting the journalized amounts to accounts in the general, preparing an unadjusted trial balance, perhaps preparing a worksheet, formative and recording adjusting entries, preparing an adjusted trial balance, preparing the financial statements, recording and posting closing entries, preparing a post-closing trial balance, and perhaps recording reversing entries.

To establish the correctness of the work done, these balances are transferred to a statement called trial balance. Preparation of trading and profit and loss account is the next step. The balancing of profit and loss account gives the net result of the business transactions. To know the financial position of the business concern balance sheet is prepared at the end.

These transactions which have finished the present accounting year, once again come to the starting point – the journal – and they move with new transactions of the next year. Thus, this cyclic movement of the transactions through the books of accounts (accounting cycle) is a continuous process.