Dual Aspect Concept, also known as Duality Principle, is a fundamental convention of accounting that necessitates the recognition of all aspects of an accounting transaction. Dual aspect concept is the underlying basis for double entry accounting system.

Contents:

- Definition

- Explanation

- Example

Explanation

In a single entry system, only one aspect of a transaction is recognized. For instance, if a sale is made to a customer, only sales revenue will be recorded. However, the other side of the transaction relating to the receipt of cash or the grant of credit to the customer is not recognized.

Double entry accounting system is based on the duality principle and was devised to account for all aspects of a transaction. Under the system, aspects of transactions are classified under two main types:

- Debit

- Credit

Debit is the portion of transaction that accounts for the increase in assets and expenses, and the decrease in liabilities, equity and income.

Credit is the portion of transaction that accounts for the increase in income, liabilities and equity, and the decrease in assets and expenses.

Examples:

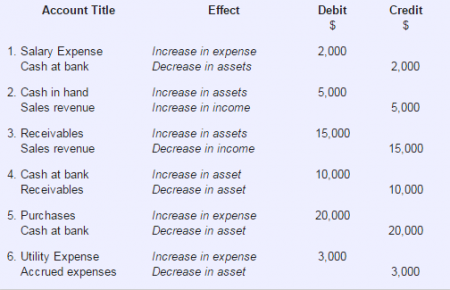

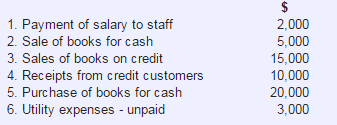

Mr. A, who owns and operates a bookstore, has identified the following transactions for the month of January that need to be accounted for in the monthly financial statements:

Under double entry system, the above transactions will be accounted for as follows: