Final accounts are a rather outdated bookkeeping term that refers to the final trial balance at the end of an accounting period from which the financial statements are derived. This final trial balance includes the whole journal entries used to close the books, such as Wage and payroll tax accruals.

Trial balance proves the mathematical correctness of the trade transactions, but it is not the end. The businessman is concerned in knowing whether the business has resulted in profit or loss and what the financial position of the business is at a given period. In short, he wants to know the prosperity and the economic reliability of the business. The trader can determine these by preparing the final accounts. The final accounts are organized at the end of the year from the trial balance. Hence the trial balance is said to be the relating link between the ledger accounts and the final accounts.

Parts of Final Accounts

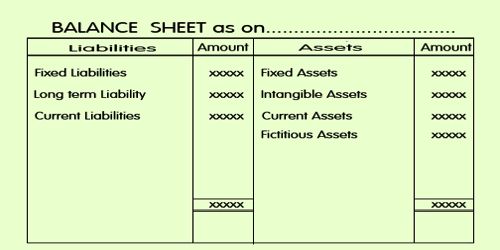

The final account of business apprehension usually includes two parts. The first part is Trading and Profit and Loss Account. This is organized to find out the net outcome of the business. The second part is Balance Sheet which is arranged to know the financial situation of the business. However industrialized concerns, will prepare a industrialized Account prior to the preparation of trading account, to find out cost of production.