Dividend Coverage Ratio states the number of times an organization is capable of paying dividends to shareholders from the profits earned during an accounting period.

Formula

Dividend cover in respect of ordinary share capital may be calculated as follows:

![]()

Explanation

Dividend Coverage Ratio indicates the capacity of an organization to pay dividends out of profit attributable to the shareholders. A dividend cover of 3 implies that a company has sufficient earnings to pay dividends amounting to 3 times of the present dividend payout during the period.

Example

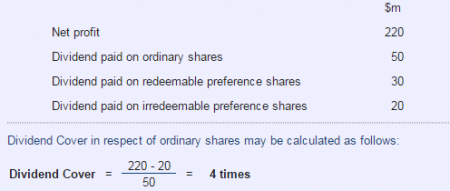

The following information relates to the financial statements of ABC PLC for the year ended 31st December 2012:

As dividend paid on redeemable preference shares would have been already accounted for in arriving at the net profit of ABC PLC, no further adjustment is required in the calculation of earnings attributable to ordinary shareholders.

Interpretation & Analysis

Dividend Coverage is a measure of the ability of an organization to pay dividends. Although dividend payments are usually discretionary, companies normally seek to maintain a reasonable level of dividend payout in line with the market expectations.

Generally, companies would aim to sustain a dividend cover of at least 2 times in order to avail adequate financing through retained earnings while providing a reasonable cash return on shareholder’s investment. A higher or lower dividend cover may be appropriate depending on the level of stability in earnings of the organizations.

Dividend cover consistently below 1.5 may suggest that the company might not be able to maintain the present level of dividends in case of adverse variation in profit in the future.