Elements of Cost of manufacturing Product

In the manufacturing industry, cost accounting is a fundamental requirement for achieving success. To be competitive and profitable, a manufacturer must understand and control the three basic elements of manufacturing costs – direct materials, direct labor and factory overhead.

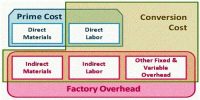

(a) Direct materials consist of all of the materials that become an integral pail of the finished product. Direct materials should include the actual cost of the materials, as well as freight in, import duties, purchasing costs, receiving costs, storage costs and other directly attributable costs of acquiring the materials. Direct Materials should be recorded net of any trade, quantity or cash discounts attributed to the materials.

(b) Direct labor consists of all of the personnel costs required to manufacture the finished product. Direct labor should include wages, payroll taxes, and benefits associated with personnel who are integral to manufacturing the finished product.

(c) Factory overhead consists of all of the other costs required to manufacture the finished product that does not fit into the direct material or direct labor elements. They consist mainly of indirect material, indirect labor, depreciation, utilities, rent, repairs and maintenance, and insurance.

In the current economic conditions, companies have been searching for ways to improve efficiencies, in order to maintain profitability and a competitive advantage. Phase one of this effort should be to perform an operational assessment to identify the strengths and key deficiencies within the manufacturing process. The assessment would include a detailed review and analysis of manufacturing areas such as service and quality, management and personal abilities, reporting metrics and systems, inventory management and plant physical layout. The assessment exposes areas within the manufacturing process that can be used to initiate and concentrate improvement efforts and cost reduction strategies. Cutting costs prior to performing an operational assessment might not result in improved efficiency or profitability.