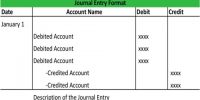

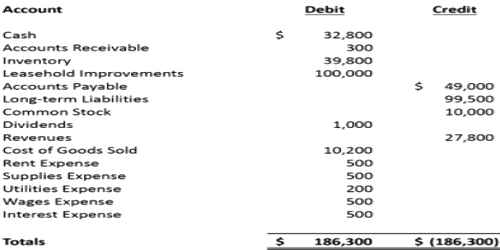

The trial balance is an account which shows debit balances and credit balances of all accounts in the ledger. It is a statement of all debts and credits in a double-entry account book, with any disagreement signifying a fault. Since every debit should have a consequent credit as per the rules of double entry system, the total of the debit balances and credit balances should tally (agree). In case, there is a dissimilarity, one has to check the correctness of the balances brought forward from the individual accounts. The trial balance can be equipped with any date provided accounts are balanced.

Definition

“Trial balance is a statement, prepared with the debit and credit balances of ledger accounts to test the arithmetical accuracy of the books” – J.R. Batliboi.

In a handbook structure, a trial balance was usually prepared by the bookkeeper in order to find out whether arithmetic mistakes and/or some posting faults were made. Today, bookkeeping and accounting software have got rid of those accounting mistakes. This means that the trial balance is fewer vital for bookkeeping purposes since it is nearly assured that the total of the debt and credit columns will be equivalent.