Analytical Petty Cash Book

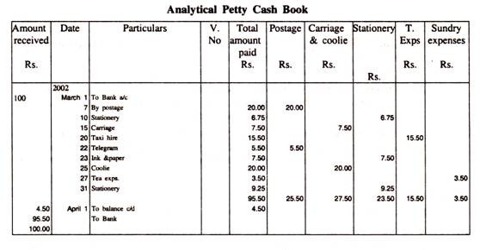

In big business apprehensions, the petty cash book is maintained in analytical form, with a detached column for each standard item of expense and a column for the total. This kind of Petty Cash Book is known as Analytical Petty cash Book. This kind enables the businessman to know the information about the amount being spent on each head of petty expense. The credit side is bigger and thus has many columns. For each significant petty expense, there is a detach column, and therefore columnar cash book is another name for this petty cash book. These analytical columns help to know the actual amount spent on each and every type of petty expenses for the particular time. Each petty payment is first entered in the whole payments column, and then recorded in the respective analytical column, so that:

- the total amount spent on each expense for a particular period can be simply ascertained by adding up the particular column.

- only the periodical total of each column is posted to the ledger.

- the total petty payment for any period can be simply ascertained from the total payments column.

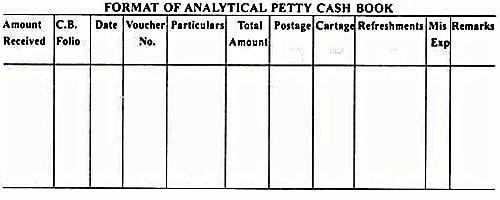

Fig: Sample format of Analytical Petty Cash Book

Other than the usual petty cash book, which resembles a regular cash book, there are two other types of petty cash books. This form enables the manufacturer to know the information regarding the total being exhausted on each head of petty expenditure. One such kind is the analytical petty cash book. In such a cash book there are pre-existing columns for the common expenses that recur moderately for an organization. Analytical Petty Cash Book also known as Columnar Petty Cash Book is dissimilar from the easy petty cash book in the logic that in this kind of petty cash book, an analytical arrangement of cash payment is prepared. So if an organization has daily fixed cost for food, stationery, postage, etc. these will be individual columns in the petty cash book.

All petty payments are to be classified into diverse heads and dissimilar columns are maintained. In the analytical version, a dividing column is used for every normally stirring item of spending such as stamps, postage, and handling, stationery, wages, etc. In this type, a dividing column for every petty expenditure is provided on credit side. When a petty expenditure is recorded on the right-hand side of the book, a similar amount is also recorded in the appropriate expenditure column. When the petty expense is recorded in entirety payment column, a similar amount is recorded in the appropriate petty cost column.

The analytical petty cash book may be designed according to the requirements of the business.

Advantage

One main advantage of this analytical system is that it saves time. It is the most advantageous method of recording petty cash payments. Also, it will facilitate the accountant or the organization to evaluate the operating cost under the dissimilar various heads. It also saves time in posting every item of petty payments needlessly in the ledger; only totals of diverse columns are to be posted in the ledger. This makes comparisons easier as well.