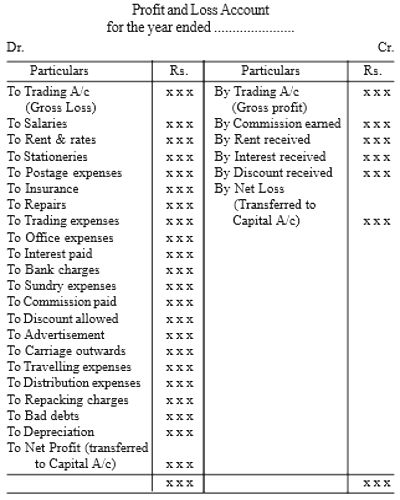

Format of Profit and Loss Account

Profit and loss accounts show your total income and expenses, and also shows whether your business has earned more income than it has spent on its running costs. If that is the case, then your business has made a profit. This account shows what net profit or loss your business has made within an accounting period after deducting all expenditure from income. A net profit is earned if total expenditure is less than the sales and a net loss if it is greater.

Items appearing in the debit side

Those expenses which are chargeable to the normal activities of the business are recorded in the debit side of profit and loss account. They are termed as indirect expenses.

- Office and Administrative Expenses: Expenses incurred for the functioning of an office are office and administrative expenses – office salaries, office rent, office lighting, printing and stationery, postages, telephone charges etc.

- Repairs and Maintenance Expenses: These expenses relates to the maintenance of assets – repairs and renewals, depreciation etc.

- Financial Expenses: Expenses incurred on borrowings – Interest paid on loan.

- Selling and Distribution Expenses: All expenses relating to sales and distribution of goods – advertising, travelling expenses, salesmen salary, commission paid to salesmen, discount allowed, repacking charges etc.

Items appearing in the credit side

Besides the gross profit, other gains and incomes of the business are shown on the credit side. The following are some of the incomes and gains.

- Interest received on investment

- Interest received on fixed deposits.

- Discount earned.

- Commission earned.

- Rent Received