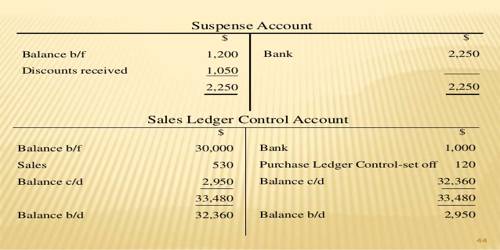

A suspense account is an account in the general ledger in which amounts are provisionally recorded. When it is hard to find the faults before preparing the final accounts, the dissimilarity in the trial balance is transferred to newly open imaginary and provisional account called ‘Suspense Account’. Suspense account is prepared to keep away from the delay in the preparation of final accounts. If the total debit balance of the trial balance exceeds the total credit balances, the dissimilarity is transferred to the credit side of the suspense account. On the other hand, if the total credit balances of the trial balance exceeds the total debit balances the difference is transferred to the debit side of the suspense account. The suspense account is used because the appropriate account could not be determined at the time that the transaction was recorded.

When the errors affecting the suspense account are located, they are rectified with suspense account. Suspense account is continued in the books until the errors are located and rectified. Such balance will be shown in the balance sheet. Debit balance will be shown on the asset side and the credit balance will be shown on the liability side. When all the errors affecting the trial balance are located and rectified, the suspense account automatically gets closed.