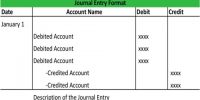

A Trial Balance is a statement that shows the total debit and total credit balances of accounts. It is like a bookkeeping worksheet the company prepares at the end of the financial year. The total of debit amounts shall be equal to the credit amounts. Basically, it is an account that lists the closing balance of each account on the respective debit or credit side. It thus verifies the arithmetical accuracy of the postings in the ledger accounts. One of the main objectives of the trial balance is to ensure that the total of all debits equals the total of all the credits.

Preparing the trial balance is the third step of the accounting process. After journalizing and posting all entries in the ledgers, the bookkeepers prepare the trial balance. The general purpose of producing a trial balance is to ensure the entries in a company’s bookkeeping system are mathematically correct.

Objectives of Trial Balance

Trial Balance proceeds as the first step in the preparation of financial statements. It is a working paper that accountants use as a foundation while preparing financial statements. It assists in the recognition and modification of faults. In a manual structure, a trial balance was usually organized by the bookkeeper in order to determine whether math faults and/or some posting errors were made. Today, bookkeeping and accounting software have got rid of those clerical mistakes.

The trial balance is prepared to achieve the following objectives:

(i) To ascertain arithmetical accuracy: It ensures that both aspects of every transaction have been posted into ledger i.e., debit aspect of the transaction on the debit side and the credit aspect of the transaction on credit.

(ii) To facilitate detection of errors: Trial balance helps in locating errors committed during ledger posting.

(iii) To facilitate the preparation of financial statements: Trial Balance contains all ledger accounts, and provides a basis for further processing of accounting data i.e. preparation of financial statements.

(iv) To facilitate auditors: Agreement of trial balances assures Auditors that all transactions have been recorded in books of

The other objectives of preparing a trial balance are:

- To verify the mathematical correctness of the ledger accounts.

- To find the faults.

- To make possible the preparation of the final financial statement.

Advantages

The advantages of the trial balance are –

- It presents to the businessman a consolidated list of all ledger balances.

- It assists to determine the mathematical correctness of the book-keeping work done during the period.

- It is the shortest method of verifying the arithmetical accuracy of entries made in the ledger.

- It supplies in one place prepared reference of all the balances of the ledger accounts.

- If the total of the debit side/column is equal to the total of the credit side/column, the trial balance is said to agree. Otherwise, it is implied that some errors have been committed in the preparation of accounts.

- If any fault is found out by preparing a trial balance, the same can be rectified before preparing final accounts.

- It helps in the preparation of the final accounts i.e., Trading a/c. Profit and loss a/c and Balance Sheet.

- It is the foundation on which final accounts are organized.