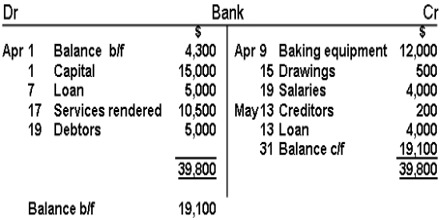

Balancing an Account

Balance is the diversity of the total debits and the total credits of an account. When posting is complete, many accounts may have entries on their debit side as well as credit side. The net result of such debits and credits in an account is the balance. This is the majority significant division of an account as it shows value or place of asset, liability, capital, income or expenses of which the account is a record.

Balancing means the writing of the diversity between the amount columns of the two sides in the lighter (minor total) side so that the grand totals of the two sides become equivalent. The account balance is constantly the net amount after factoring in all debits and credits.

Reasons for Balancing Accounts:

There is no rigid and fast rule; however, the requirement for balancing an account might occur when:

(1) The accessible page due for the account is full and balance is necessary to be calculated and transferred to the subsequently page.

(2) Business has requirements information for a particular item for which an account already exists.

(3) Trial balance is being organized for which accounts’ balances are required for its preparation.