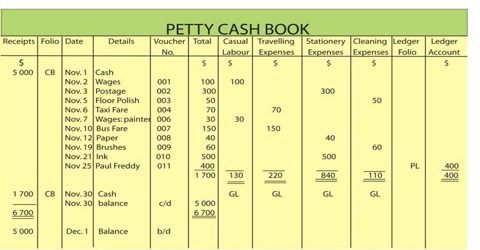

Imprest System of Petty Cash Book

Imprest means ‘money advanced on loan’. This method is a structure of financial accounting system. The most general imprest system is the petty cash system. Under this method, the amount essential to assemble out various petty operating costs is estimated and given to the petty cashier at the beginning of the particular time, generally a month. All the expenditure is supported by vouchers. At the end of the given time or before, when the petty cashier has exhausted the petty cash amount, he closes the petty cash book for the time and balances it. Then he submits the accounts to the cashier. He verifies the petty cash book with the vouchers. After agreeable himself as to the accuracy of the payments, an amount equivalent to the cash spent is given to the petty cashier. This amount together with the unspent amount will bring up the cash in hand to the amount with which he originally started i.e., the imprest amount. Thus the method of reimbursing the amount spent by the petty cashier at a fixed time is known as the imprest system of petty cash.

The important features of an imprest system are:

- A fixed amount of cash is to be paid to a petty cash account, which is stated in a divide account in the general ledger.

- All cash distributions from the petty cash fund are documented with receipts.

- Petty cash costs receipts are used as the basis for periodic replenishments of the petty cash fund.

- Variances between expected and actual fund balances are regularly reviewed and investigated.

Due to grow of electronic transactions, the imprest system is becoming less common. Many businesses now desire to use credit cards for minor purchases or to inquire workers to pay in cash then be appropriate for repayment.