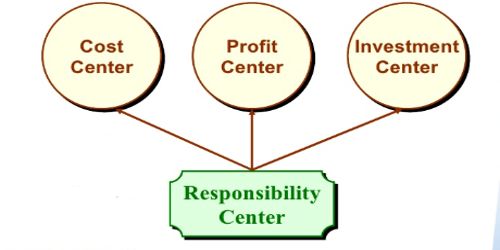

It is important to monitor the performance of cost, profit and investment centre to judge how both the centre are performing economically and how their managers are performing as managers. It is important not to judge managers for elements of performance for which they have no responsibility.

Performance measures for Profit centre include:

The manager of a profit center has control met both cots and revenue. Managers of profit centers are evaluated on their ability to control costs as well as their ability to generate revenue and profits in their departments.

Profit compared to budget: Profit centre will usually have budgets to work to so this simple comparison is very useful.

Profit per unit: because a profit centre manager is responsible for costs and revenues, profit per unit produced or supplied is an obvious measure. A simple way to calculate this is to divide the profit for a period by the units produced in the period.

Gross profit percentage: this is the gross profit divided by sales and expressed as a percentage. It shows how many $ of gross profit are generated by each $ of sales. Gross profit can be thought of as the mainspring of profit generation.

Net profit percentage: this is the net profit divided by sales and expressed as a percentage.

Expenses/sales: these can be useful ratios to see if expenses (such as administration expenses) are keeping in line with sales.