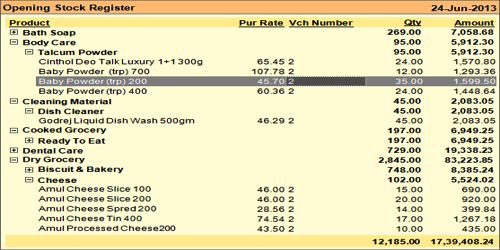

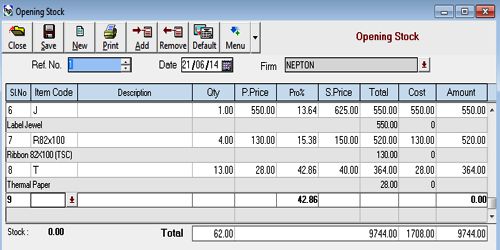

Opening Stock:

Opening stock consists of raw materials; work in improvement and finished goods depending upon the character of business. It is the worth of goods accessible for sale in the opening of an accounting period. In merchandising business, the opening stock consists of finished goods. In industrialized apprehension, opening stock consists of raw materials.

Here cost of goods sold is not just the cost of purchases throughout the period. This is the function of the Matching Concept which requires expenses to be recognized against periods from which related revenue from the expense is expected to be earned. Therefore, as closing inventory is not consumed at any given accounting period end, it must not be element of expense which is why it is deducted from the cost of sale. Likewise, as opening inventory is consumed in the current accounting period, it must therefore be added to the cost of goods sold.