Ways of Lowering the Break-Even Point Ways of Lowering the Break-Even Point Break-even point is that level of operation at which sales revenues for a period are equal to the costs…

An increase in Income Tax Rate affects the Break-Even Point – Explanation An increase in Income Tax Rate affects the Break-Even Point An increase in the income tax rate does not affect the breakeven point. Operating income…

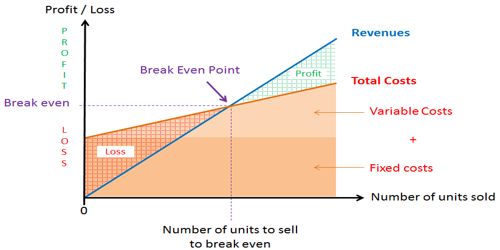

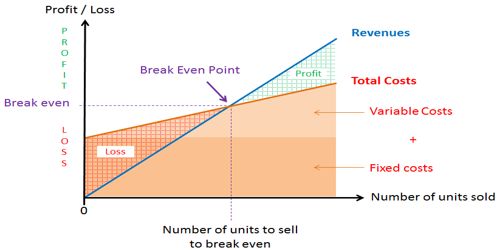

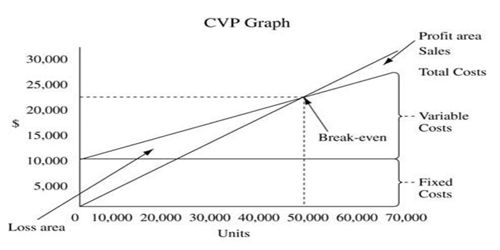

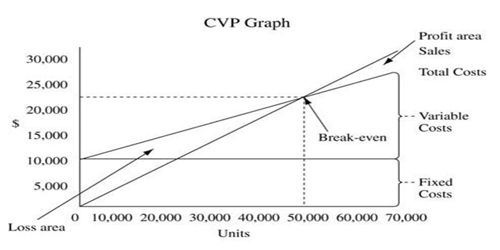

Uses of CVP Analysis Cost-volume-profit (CVP) analysis is used to determine how changes in costs and volume affect a company’s operating income and net income. CPV analysis is a…

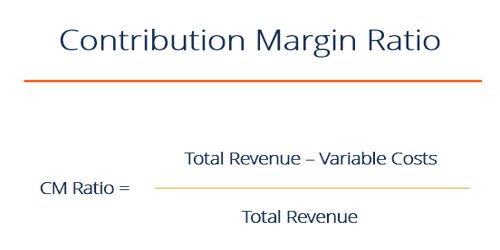

Product’s Contribution Margin Ratio Product’s Contribution Margin Ratio: Product Contribution margin ratio is commonly expressed as a percentage of sales prices. It is the difference between a company’s sales…

Absorption costing considers more categories of costs a product cost – Explain “Absorption costing considers more categories of costs a product cost” Absorption costing, also known as full costing is a method by which all of the…

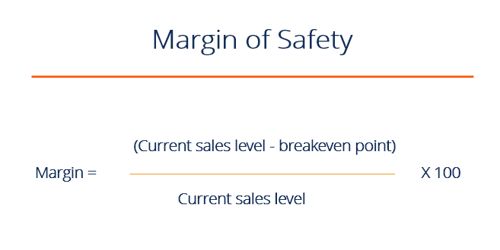

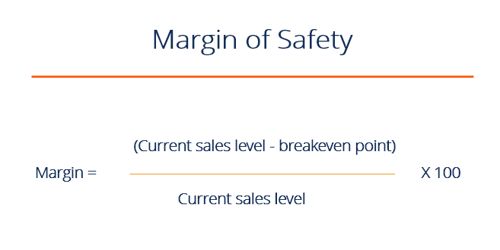

Significance of Margin of Safety The significance of Margin of Safety The margin of safety establishes the surplus of actual sales earnings over and above the break-even earnings. The excess…

Margin of Safety Ratio (M/S Ratio) The margin of Safety Ratio (M/S Ratio) The excess of actual or budgeted sales over the break-even volume of sales is called the margin of…

Cost Volume Profit (CVP) Analysis CPV analysis is a powerful tool that helps managers understands the relationships of cost volume and profit. Cost volume profit (CVP) analysis is the relationship…

Usages of Variable Costing in Decision Making Usages of variable / direct costing in decision making: Under variable costing, only those manufacturing costs that very without put are treated as product costs.…

Why is manufacturing overhead considered an indirect cost of a unit of products? Manufacturing overheads are indirect costs of a product. If they are direct costs, they won’t be termed overheads. Manufacturing overhead (also referred to as factory…