The significance of Margin of Safety

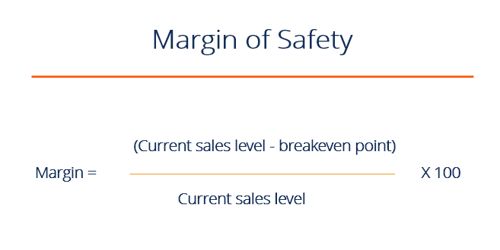

The margin of safety establishes the surplus of actual sales earnings over and above the break-even earnings. The excess of actual or budgeted sales over the break-even volume of sales is called the margin of safety. It is a financial ratio that measures the number of sales that exceed the break-even point. In break-even analysis, the margin of safety is the extent by which actual or projected sales exceed the break-even sales. The formula for calculating the margin of safety is: (Actual Sales – Break-even Sales Earnings).

Companies use the margin of safety in management accounting to establish the strength and potency of the business. The higher the margin of safety, the sturdier it deems business. A high margin of safety indicates the soundness of business i.e., the break-even point is much below the actual sales so that even if there is a fall in sales, there will still be a profit. A small margin, on the other hand, indicates a not-too-sound position. If a low margin of safety is accompanied by high fixed cost and high contribution margin ratio, an action is called for reducing the fixed cost or increasing sales volume. A low margin of safety is a matter of concern and so the following steps may be taken to improve an unsatisfactory margin of safety:

- Increase the selling price

- Reduce the fixed or variable costs or the both.

- Increase the volume of output by utilizing the unutilized production capacity.

- Stop production of unprofitable products and concentrate on only the profitable products.

Companies attempt to place their selling price at such a point in order to cover fixed and variable costs. So it is an important figure for any business because it tells management how much reduction in revenue will result in break-even.