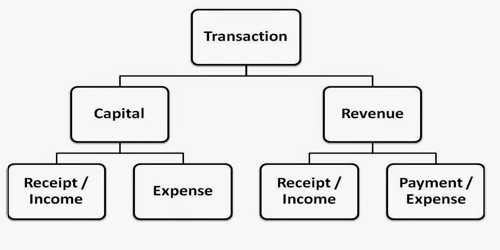

Capital Transactions

The business transactions, which provide advantages or supply services to the business apprehension for more than one year or one operating sequence of the business, are known as capital transactions. These types of transactions affecting non-current items such as fixed assets, long-term debt or allocate capital, rather than revenue transactions

The transactions which relate to capital are again sub-divided into capital expenditure and capital receipt. It is one that deals with non-current assets or liabilities.

Once the trial balance is prepared the next step is to find out the net result (profit or loss account) and financial position (balance sheet) of the business concern. The business concern’s financial position is bound to be affected by the result of its operations. ‘Matching Principle’ governs the preparation of these two statements. According to this principle, the revenues and relevant expenditures incurred during a particular period should be matched.

A capital transaction is one that deals with non-current assets or liabilities, such as:

- fixed assets (ex. buying and selling equipment),

- certain kinds of investments (ex. the buying and selling of securities intended to be held for long-term investment),

- long-term debt (ex. the acquisition and paying off of loans that have terms longer than one year), and

- equity transactions (ex. dividend payments and share purchases)