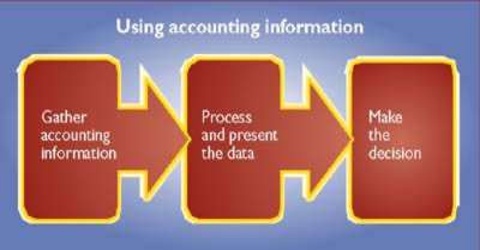

Qualitative Distinctiveness of accounting information

The following are the qualitative distinctiveness of accounting information:

- Relevance- It means that necessary and suitable information should be effortlessly and timely obtainable and any unrelated information should be avoided. Relevance accounting information is the compilation of a company’s financial dealings. The users of accounting information need related information for decision making, planning and predicting the potential circumstances.

- Reliability- Reliability is the excellence of information that approved users to depend on it with assurance. It means that the user can rely on the accounting information. All accounting information is confirmable and can be confirmed from the source document (voucher), viz. cash memos, bills, etc. Hence, the obtainable information should be free from any errors and impartial.

- Comparability- It is the majority vital quality of accounting information. Comparability means accounting information of a present year can be similar with that of the preceding years. Comparability results when dissimilar enterprises apply the similar accounting management to similar events. Compliance with international accounting standards helps to improve comparability

- Understandability– Accounting information should be presented in such a way that every user is able to understand the information without any complexity in a significant and suitable way.

Further, it helps to determine the growth and development of the business over time and in assessment to other businesses.