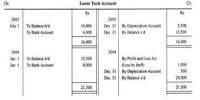

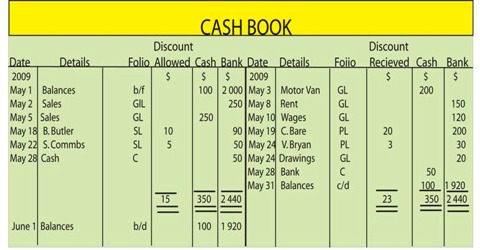

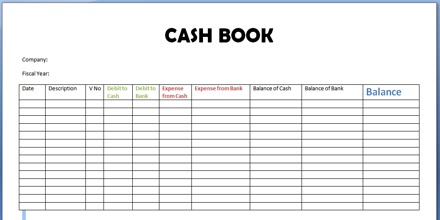

A cash book is a exceptional journal which is used to record all cash receipts and cash payments. It is a financial journal that contains all cash receipts and payments, including bank deposits and withdrawals. The cash book is a book of unique entry or prime entry since transactions are recorded for the initial time from the source documents. The cash book is a ledger in the sense that it is designed in the form of a cash account and records cash receipts on the debit side and cash payments on the credit side.

Thus, the cash book is both a journal and a ledger. Cash Book will constantly show debit balance, as cash payments can never exceed cash accessible. In short, cash book is a particular journal which is used for recording all cash receipts and cash payments. Entries in the cash book are then posted into the general ledger. It plays a double function. It is both a book of original entry as well as a book of final entry. It always shows debit balance. It can never show credit balance.