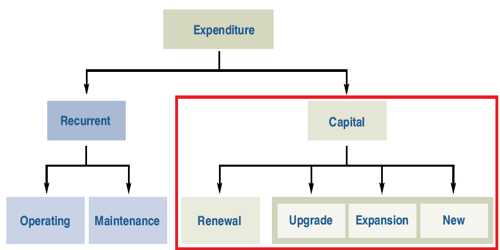

Capital expenditure consists of those expenditures, the advantage of which is carried over to quite a few accounting periods. In other words the advantage of which is not consumed within one accounting period. It is non-recurring in character. Capital expenditure is funds used by a company to obtain or upgrade physical assets such as property, industrial buildings or equipment.

The amount of capital expenditures for an accounting period is reported in the cash flow statement. The amount is an outflow of cash and is listed in the investing activities section of the statement. Sometimes the amount is listed as capital expenditures and sometimes it is listed as purchase of property and equipment.

Characteristics

In other words, it refers to the expenditure, which may be

- purchase of a fixed asset.

- not acquired for sale.

- it is non-recurring in character.

- incurred to increase the operational efficiency of the business concern.

Examples

- Expenses incurred in the acquisition of Land, Building, Machinery, Furniture, Car, Goodwill, Copyright, Trade Mark, Patent Right, etc.

- Expenses incurred for increasing the seating accommodation in a cinema hall.

- Expenses incurred for installation of fixed assets like wages paid for installing a plant.

- Expenses incurred for remodelling and reconditioning an existing asset like remodeling a building.