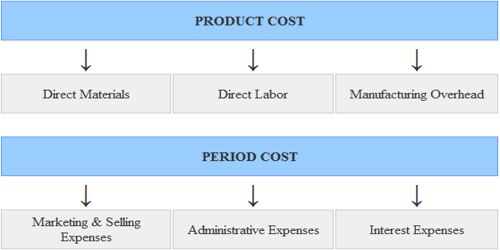

Product cost refers to the costs used to create a product. These costs include direct labor, direct materials, consumable production supplies, and factory overhead. The period costs are usually associated with the selling function of the business or its general administration. Examples of these costs include office rent, interest, depreciation of office building, sales commission, and advertising expenses etc.

The difference between product cost and period cost are as follows –

Product Costs:

- The cost that can be apportioned to the product is known as Product Cost.

- Cost identified with goods produced or purchased for resale.

- Products costs are initially identified as part of the inventory on hand.

- In manufacturing accounting, many of those items are relayed to production activities and thus, as indirect manufacturing are product costs.

- Become expenses in the form of costs of goods sold as the inventory is sold.

- Cost of raw material, production overheads, depreciation on machinery, wages to labor, etc.

Period Costs:

- The cost that cannot be assigned to the product, but charged as an expense is known as Period cost.

- Costs that are deducted as expenses during the current period without going through an inventory stage.

- Period costs are identified expenses during the current period.

- In Merchandising and manufacturing accounting, selling and general administrative costs are period costs.

- Expenses for the current Period.

- Salary, rent, audit fees, depreciation on office assets etc.