The margin of Safety Ratio (M/S Ratio)

The excess of actual or budgeted sales over the break-even volume of sales is called the margin of safety. It is a financial ratio that measures the number of sales that exceed the break-even point. In break-even analysis, the margin of safety is the extent by which actual or projected sales exceed the break-even sales. It may be calculated simply as the difference between actual or projected sales and the break-even sales. However, it is best to calculate a margin of safety in the form of a ratio. Thus we have the following two formulas to calculate a margin of safety:

MOS = (Budgeted Sales – Break-even Sales)

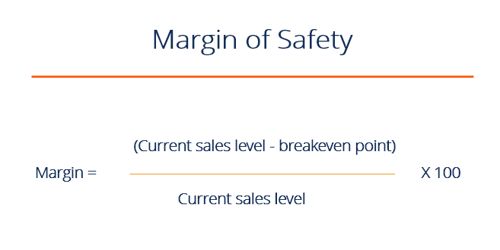

The margin of safety can also be expressed in percentage form (Margin of safety ratio). This percentage is obtained by dividing the margin of safety into dollar terms by total sales. Following equation is used for this purpose.

MOS = [(Budgeted Sales – Break-even Sales) / Budgeted Sales]

The margin of Safety can be expressed both in terms of sales units and currency units.

The margin of safety is a measure of risk. It represents the amount of drop in sales which a company can tolerate. Higher the margin of safety, the more the company can withstand fluctuations in sales. A drop in sales greater than the margin of safety will cause the net loss for the period.

Example –

Use the following information to calculate a margin of safety:

Sales Price per Unit $40

Variable Cost per Unit $32

Total Fixed Coot $7,000

Budgeted Sales $40.000

Solution

Breakeven Sales Units = $7,000 / ($40 – $32) = 875

Budgeted Sales Units = $40,000 / $40 = 1,000

Margin of Safety = (1000 – 875) /1,000 = 12.5 %

Companies use the margin of safety in management accounting to establish the strength and potency of the business. The higher the margin of safety, the sturdier it deems business. Companies attempt to place their selling price at such a point in order to co fixed and variable costs.