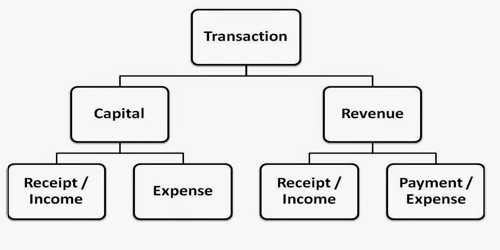

Revenue Transactions Revenue Transactions are a transaction that is generally of a short-term nature and is only expected to benefit the current period. Revenue transactions appear in…

Capital Transactions Capital Transactions The business transactions, which provide advantages or supply services to the business apprehension for more than one year or one operating sequence of…

Capital Expenditure Capital expenditure consists of those expenditures, the advantage of which is carried over to quite a few accounting periods. In other words the advantage of…

Capital Receipt Capital receipt is one which is invested in the business for a long period. It includes long term loans obtained from others and any amount…

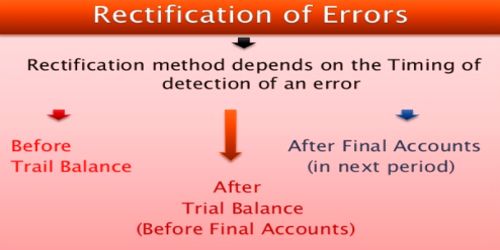

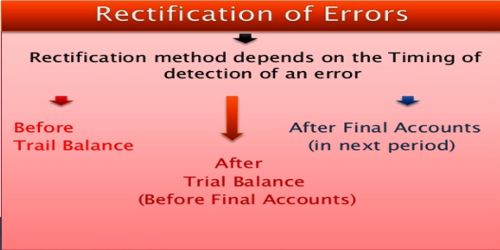

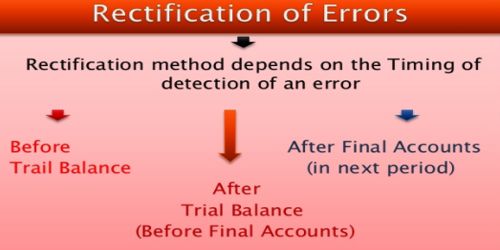

Stages of Rectification of Errors Stages of Rectification The stage in which rectification is done depends on identification or locating the error. Rectification of errors may be explained in two…

Basic Principles for Rectification of Errors Basic Principles for Rectification of Errors Correcting the errors that has occurred is called Rectification. Proper entry is conceded or appropriate descriptive note is written…

Rectification of Errors in Accounting Rectification of Errors Correction of errors in the books of financial records is not finished by erasing, rewriting or striking the figures which are incorrect.…

Suspense Account A suspense account is an account in the general ledger in which amounts are provisionally recorded. When it is hard to find the faults before…

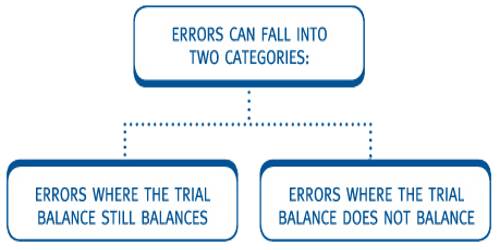

Steps to find the Errors in Trial Balance Steps to find the Errors in Trial Balance: If the trial balance does not tally, it means there are various errors in the books of…

Errors of Omission Errors of Omission This error happens when a transaction is totally or partly omitted to be recorded in the books of accounts. The accountant’s major…