Distinction between Journal and Ledger Distinction between Journal and Ledger: Books of original entry (Journal) and Ledger can be distinguished as follows: Journal Book: It is the book of prime…

Procedure for Balancing an Account Procedure for Balancing an Account While balancing an account, the following steps are involved: Step 1: Total the amount column of the debit side and…

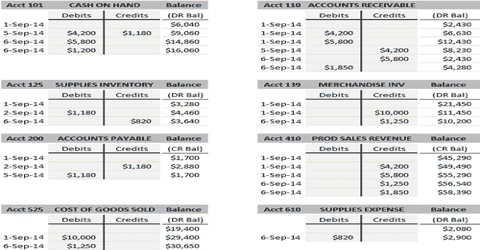

Balancing of Different Accounts Balancing of different accounts Balancing is done once in a while, i.e., weekly, monthly, quarterly, half yearly or yearly, depending on the necessities of the…

Significance of Balancing Significance of balancing Balancing means achieving equality of debit and credit totals in an account. There are three possibilities though balancing an account throughout a…

Balancing an Account Balancing an Account Balance is the diversity of the total debits and the total credits of an account. When posting is complete, many accounts may…

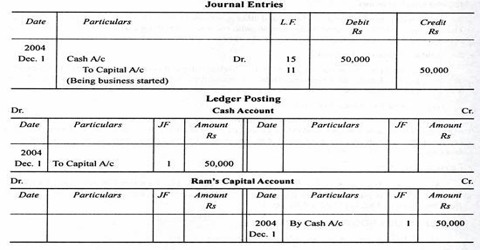

Posting the Opening Entry Posting the Opening Entry The opening entry is conceded to open the books of accounts for the new financial year. The debit or credit balance…

Procedure of Posting Ledger Procedure of Posting Ledger The procedure of posting is given as follows: Procedure of posting for an Account which has been debited in the journal…

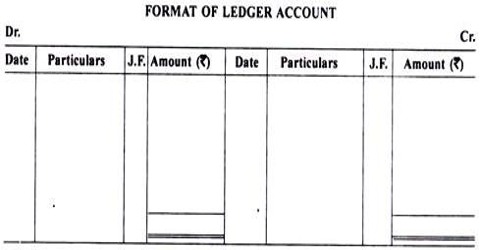

Format of Ledger Format of Ledger A Ledger is a book that includes all the accounts whether individual, real or nominal, which is primary entered in a journal…

What is Posting Ledger? Posting Ledger The process of transferring the entries recorded in the journal or subsidiary books to the respective accounts opened in the ledger is called…

Advantages of Ledger Advantages of ledger Ledger is a primary or main book which includes all the accounts in which the transactions recorded in the books of original…