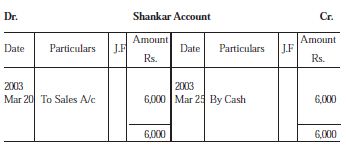

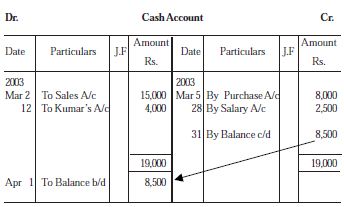

Significance of balancing

Balancing means achieving equality of debit and credit totals in an account. There are three possibilities though balancing an account throughout a certain period. It might be a debit balance or a credit balance or a nil balance depending upon the debit total and the credit total.

(i) Debit Balance: The surplus of debit total over the credit total is called the debit balance. When there is simply debit entries in an account, the amount itself is the balance of that account, i.e., the debit balance. It is primary recorded on the credit side, above the full amount. Then it is entered on the debit side, below the full amount, as the first item for the subsequently period.

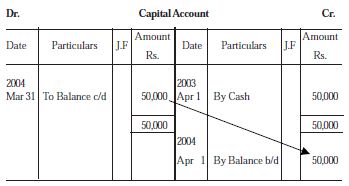

(ii) Credit Balance: The surplus of credit total over the debit total is called the credit balance. When there are simply credit entries in an account, the amount itself is the balance of that account i.e., the credit balance. It is first written in the debit side, as the last item, above the total. Then it is recorded on the credit side, below the full amount, as the first item for the subsequently period.

(iii) Nil Balance: When the total of debits and credits are equivalent, it is closed by simply writing the full amount on both the sides. It specifies the equality of benefits received and given by that account.