AccountingIrrelevance of Future Cost Irrelevance of Future Cost: In addition to pat cost, some future costs may be irrelevant because they will be the same under all feasible alternatives.…

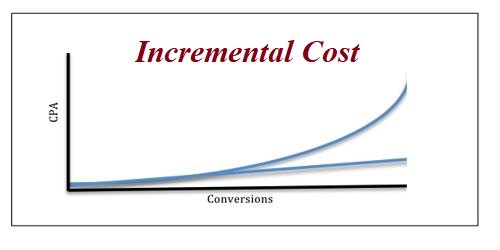

AccountingIncremental Cost Incremental cost can be defined as the encompassing changes experienced by a company within its balance sheet because of tint additional unit of production. It…

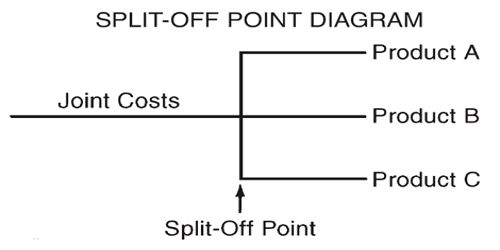

AccountingSplit-off-Point Split-off-point: The split-off point is the point in a production process where jointly manufactured products are henceforth manufactured separately; thus, their costs can be identified…

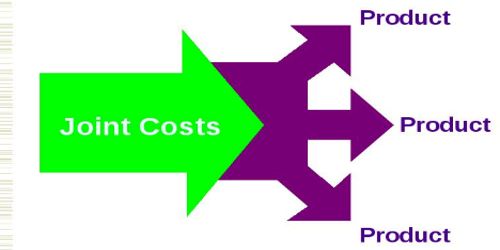

AccountingJoint Product and Joint Cost Joint Product and Joint Cost Joint product: Two or more outputs generated simultaneously, by a single manufacturing process using common input, and being substantially equal…

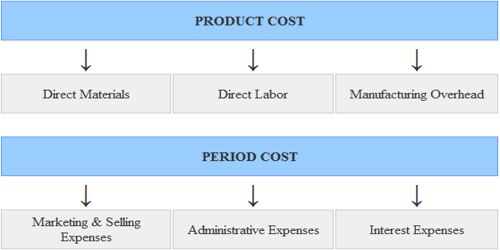

AccountingProduct Costs Product costs: For financial accounting purpose, products costs are that are involved in acquiring or making a product. In the case of manufactured goods, these…

AccountingSegment Margin in Product Line Segment Margin in Product Line Segment margin is the difference between the revenue of a segment and the direct costs of the segment represents the…

AccountingDifference between Relevant Cost and Irrelevant Cost Difference between Relevant Cost and Irrelevant Cost Relevant Cost is a cost that is pertinent to the decision being made. To be relevant, a cost…

AccountingIrrelevant Cost Irrelevant Cost: An avoidable cost is a cost that can be eliminated in whole or in part by choosing one alternative over another. These costs…

AccountingRelevant Cost Relevant Cost: A cost that is pertinent to the decision being made. To be relevant, a cost must be a future expected cost that differs…

AccountingSpecial Sales Order Special sales order: Managers must often evaluate whether a special sales order should be accepted, and if the order is accepted, the price that should…