One of the important decisions under financial management relates to the financing pattern or the proportion of the use of different sources in raising funds. The capital structure is how a firm finances its overall operations and growth by using different sources of funds. Debt comes in the form of bond issues or long-term notes payable, while equity is classified as common stock, preferred stock or retained earnings.

The capital structure shows the composition of a group’s liabilities as it shows who has a claim on the group’s assets and whether it is a debt or equity claim. The leverage ratio is the proportion of the group’s liabilities that is financed by debt claims.

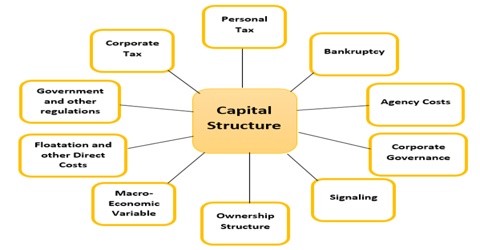

Capital structure refers to the mix between owners and borrowed funds. These shall be referred as equity and debt in the subsequent text. It can be calculated as debt-equity ratio (Debt/ Equity) or as the proportion of debt out of total capital i.e., [Debt/ (Debt +Equity)]

Debt and equity differ significantly in their cost and riskiness for the firm. Cost of debt is lower than cost of equity for a firm because lender’s risk is lower than equity shareholder’s risk, since lenders earn on assured return and repayment of capital and, therefore, they should require a lower rate of return. Additionally, interest paid on debt is a deductible expense for computation of tax liability whereas dividends are paid out of after-tax profits. Increased use of debt, therefore, is likely to lower the overall cost of capital of the firm provided that cost of equity remains unaffected.