Consumer surplus is defined as the difference between the consumers’ willingness to pay for a commodity and the actual price paid by them or the equilibrium price.

The total utility of a good is the sum of the successive marginal utilities of each added unit. Therefore, the price a peon pass for a good never exceeds, and seldom equals, that which he or she would be tilling to pay rather than go without the desired object. Only at the margin will price generally match a person willingness to pay. Thus, the total satisfaction a person gets from purchasing successive units of a good exceeds the sacrifices required to pay for the good is called consumer’s surplus.

So, finally, the total social surplus is composed of consumer surplus and producer surplus. It is a measure of consumer satisfaction in terms of utility.

Marshall theory of consumer surplus:

| Price | Quantity |

| 20 | 1 |

| 14 | 2 |

| 10 | 3 |

| 6 | 4 |

| 4 | 5 |

| 3 | 6 |

| 2 | 7 |

The price and quantity data show in above table is to illustrate consumer surplus. From the table that the person for whom these data apply would buy 1 goods if the price were Tk. 20, At Tk. 14 he would buy 2 goods, at Tk. 10, 3 goods, and so on. Suppose, the market price was actually Tk. 2, this consumer would buy 7 goods annually, pay Tk. 2 for each good, and spend Tk. 14. Notice, however, that the first good provides Tk. 20 worth of utility, the second Tk. 14 worth of utility, and so forth.This person’s total gain in utility from the purchase of the 7 good is thus Tk. 59 (20 ÷ 14+10+6+4+3+2).

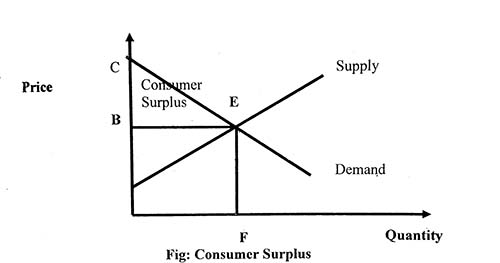

The consumer surplus is graphically shown below

Above figure shows Marshall’s Equilibrium Price and Quantity “Haggling and bargaining” of sellers and buyers result in an equilibrium price (here B) that equates quantity supplied and quantity demanded (both F). Buyers collectively receive consumer surplus of BCE.