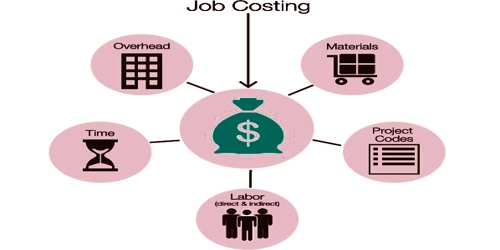

Job costing is one of the methods of costing. It is also known as job order costing. In this system, work is undertaken to customer’s specific requirements on the basis of orders. Such orders are of comparatively short duration. The work is carried out within the factory. This is usually taken as a factor to measure the feasibility of jobs. The work passes through processes or operation activities in such a way, as to identify the unit continuously until it reaches the finished product. “The term may also be applied to work such as property repairs and the method may be used in the costing of internal capital expenditure jobs.”

ICMA defines –

“Job order costing as the category of basic casting methods which is applicable where the work consists of separate contracts, jobs or batches each of which is authorized by specific order or contract.”

This method of costing is used in industries which are engaged in printing, steel structures, switchgear, heat exchangers, transformers, motors, pumps, pressure vessels, general engineering works, oil well, and shipping. It is used to amass costs at a small-unit level. For example, it is suitable for deriving the cost of constructing a routine machine, designing a software program, constructing a building, or manufacturing a little consignment of products.

Job costing is employed in industries such as Printing Press, Shipbuilding, Interior Decoration, Furniture etc.