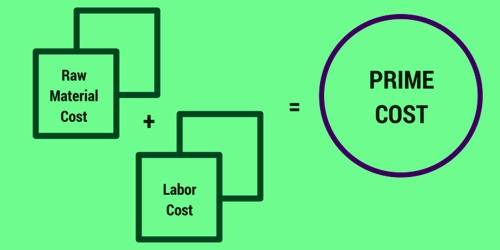

Prime cost is the combination of a manufactured product’s costs of direct materials and direct labor. In other words, prime cost refers to the direct production costs. Indirect manufacturing costs are not part of the prime cost. It refers to a manufactured product’s costs, which are calculated to ensure the best profit margin for a company. It consists of direct materials and direct labor. Direct materials include all tangible components of a product. Direct labor includes the wages paid to employees who produce finished products.

Prime Cost formula = Raw Material + Direct Labor

The prime cost calculates the use of raw materials and direct labor but does not factor in indirect expenses, such as advertising and administrative costs. It is a necessary part of total manufacturing expenses as costing and value pricing of the goods are mainly determined on its origin. Businesses use prime costs as a way of measuring the total cost of the production inputs needed to create a given output. They do not include indirect variable costs and any fixed costs.