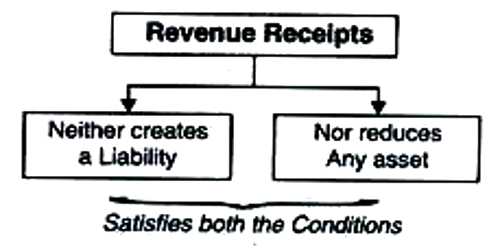

Revenue receipt is the receipt of income which is earned during the normal course of business. It is recurring in nature. It refers to those receipts which neither create any liability nor cause any reduction in the assets of the government. They are regular and recurring in nature and the government receives them in its normal course of activities. Revenue receipts include all cash inflow or amount receivables in respect of the goods sold or service rendered to the customers. Revenue receipts are also called gross income of the business firm.

Two Sources of Revenue Receipts:

Revenue receipts of the government are generally classified under two heads:

(i) Tax Revenue: Tax is a compulsory payment made by people and companies to the government without reference to any direct benefit in return.

(ii) Non-Tax Revenue: Non-Tax revenue refers to receipts of the government from all sources other than those of tax receipts.

Characteristics

- It is received in the normal course of business.

- It is recurring in nature.

Examples

- Sale of goods or services.

- Commission and Discount received.

- Dividend and interest received on investments etc.