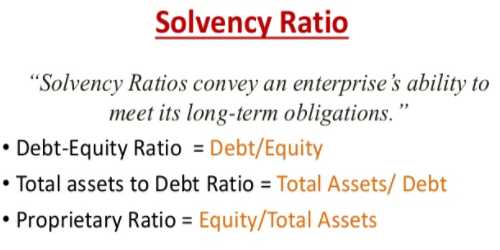

Solvency Ratios

Solvency refers to the firms’ ability to meet its long-term indebtedness. It studies the firms’ ability to meet its long-term obligations. Moreover, the solvency ratio quantifies the size of a company’s after-tax income, not counting non-cash depreciation expenses, as contrasted to the total debt obligations of the firm.

The following are the important solvency ratios:

- Debt-Equity Ratio

- Proprietory Ratio

Debt Equity Ratio

This ratio helps to ascertain the soundness of the long-term financial position of the concern. It indicates the proportion of total long-term debt and shareholders funds. This also indicates the extent to which the firm depends upon outsiders for its existence. The ratio is calculated as:

Debt-Equity Ratio = Total long-term Debt / Shareholders funds

Total long-term debt includes Debentures, long-term loans from banks and financial institutions. A shareholders fund includes Equity share capital, Preference share capital, Reserves and surplus.

Proprietory Ratio

This ratio shows the relationship between proprietors or shareholders funds and total tangible assets. The ratio is calculated as:

Proprietory Ratio = Shareholders funds (Proprietors funds) / Total tangible assets

Tangible assets will include all assets except goodwill, preliminary expenses etc.

A stronger or higher ratio indicates financial strength. In stark contrast, a lower ratio, or one on the weak side, could indicate financial struggles in the future.