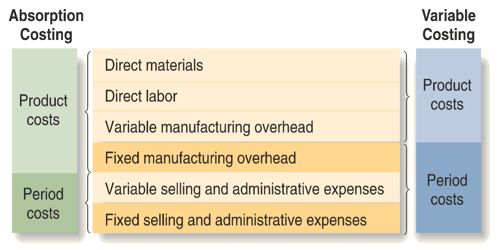

Differentiate between Absorption and Variable Costing Differentiate between Absorption and Variable Costing Absorption Costing means that all of the manufacturing costs are absorbed by the units produced. In other words, the…

Classify Costs according to managerial decision making Classify Costs according to managerial decision making Cost behavior refers to how a cost will change as the level of activity change. Costs require the…

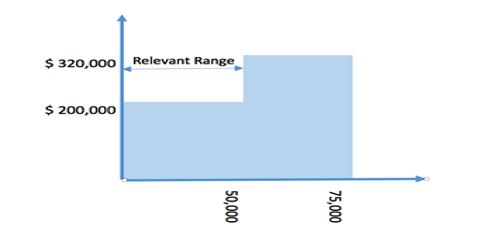

Relevant Range pertains to Fixed Costs not Variable Costs – Explanation Relevant Range pertains to Fixed Costs, not Variable Costs The relevant range refers to a particular activity level that is enclosed by a minimum and…

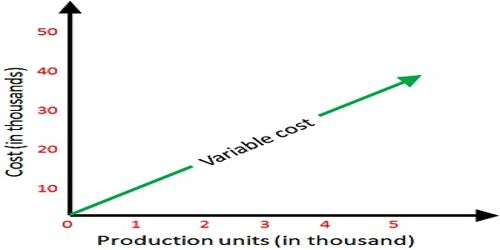

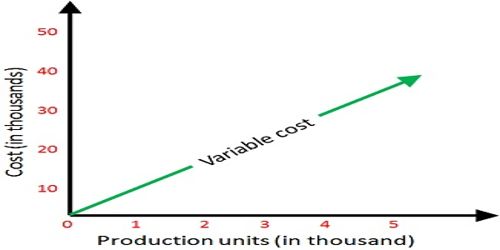

Variable Costing used only for internal reporting and not for external reporting Variable cost is constant if expressed on a per unit basis. Direct material, direct labor, and variable overhead are all variable costs. Here briefly describe…

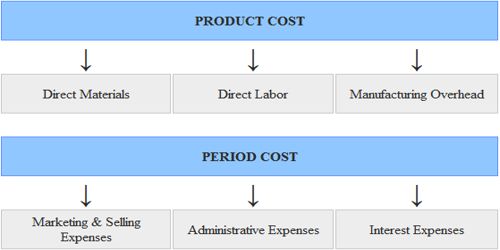

Product versus Period Cost Product versus Period Cost A manufacturer’s production costs are the direct materials, direct labor, and manufacturing overhead used in making its products. (Manufacturing overhead is…

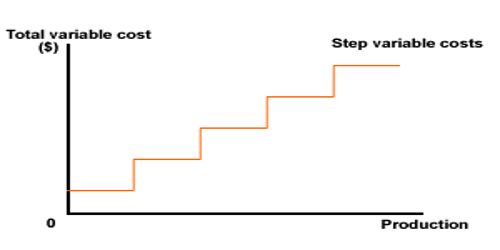

Step Variable Cost Step Variable Cost The step-variable costs are basically fixed within a narrow range but distinct increase when there are volume increases. It is a cost…

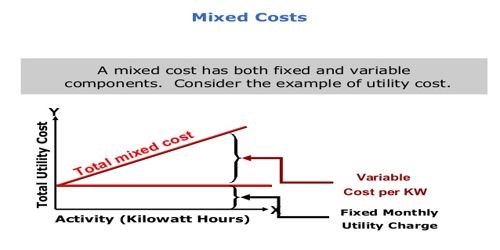

Methods of Segregating Mixed Costs Methods of Segregating Mixed Costs Mixed costs contain elements of both fixed and variable cost behavior. There are numerous methods are used for segregating mixed…

Variable Costing Variable Costing is a managerial accounting cost concept. Under this method, manufacturing overhead is incurred in the period that a product is produced. This addresses…

Absorption Costing Absorption Costing means that all of the manufacturing costs are absorbed by the units produced. In other words, the cost of a finished unit in…

How are fixed overhead costs shifted from one period to another under absorption costing? Fixed manufacturing overhead costs are monthly or annual expenses that remain constant regardless of production volume or the total number of our production equipment was…