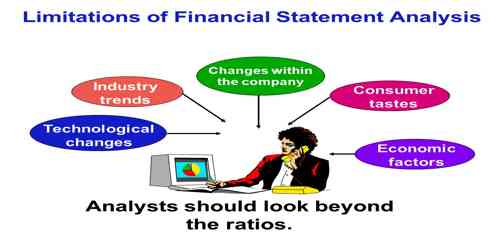

Limitations of Financial Statement Analysis

Financial statements are final result of accounting work done during the accounting period. Financial statements normally include Trading, Profit and Loss Account and Balance Sheet. It is important as it provides meaningful information to the shareholders in taking such decisions. They are also important to a company’s managers because by publishing financial statements, management can communicate with interested outside parties about its accomplishment running the company.

Analysis of financial statements helps to ascertain the strength and weakness of the business concern, but at the same time it suffers from the following limitations.

- It analyses what has happened till date and does not reflect the future.

- It ignores price level changes.

- Financial analysis takes into consideration only monetary matters, qualitative aspects are ignored.

- The conclusions of the analysis is based on the correctness of the financial statements.

- Analysis is a means to an end and not the end itself.

- As there is variation in accounting practices followed by different firms a valid comparison of their financial analysis is not possible.

- Diversified companies are difficult to classify for comparison purposes.

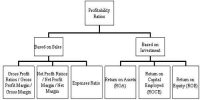

Financial statement analysis does not provide answers to all the users’ questions. In fact, it usually generates more questions! There are different ways by which financial statement analysis can be undertaken and one among them is “Ratio Analysis”.