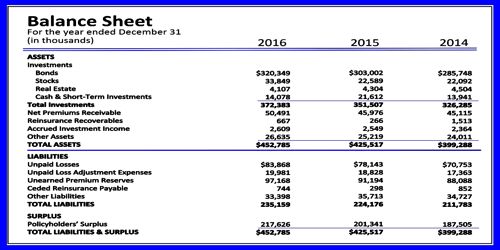

Balance Sheet is a tabular report of balances carried further after closing the books of account reserved according to principles of accounting. It is a statement arranged with a view to determine the financial situation of a business on a definite fixed date. Balance sheet indicates the financial situation of a apprehension by its assets on a given date and its liabilities on that date. Excess of assets over liabilities represents capital or net worth or shareholders’ fund and is indicative of the financial soundness of a company.

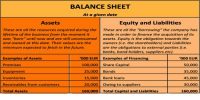

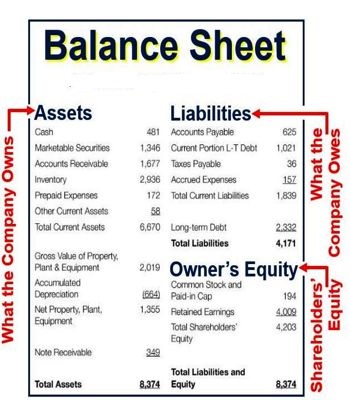

Typical line items included in the balance sheet (by general category) are:

- Assets: Cash, profitable securities, prepaid expenses, accounts receivable, inventory, and fixed assets

- Liabilities: Accounts payable, accrued liabilities, taxes payable, short-term debt, and long-term debt

- Shareholders’ equity: Stock, retained earnings, and treasury stock

The reason of the balance sheet is to provide an idea of a company’s financial situation. It does so by outlining the total assets that a company owns and any amounts that it owes to lenders or banks, for example, as well as the amount of equity.

Balance sheets do not show results, even if they can be inferred by comparing the balance of accounts from dissimilar time periods.