Double Entry System

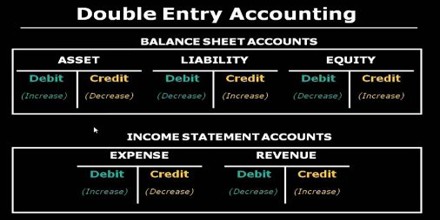

The double entry system of accounting means that each trade transaction will engage two accounts (or more). It is an accounting method that records a debit and credit for each financial operation happening within a company. In short, the essential principle of this system is, for every debit, there must be a corresponding credit of equal amount and for every credit, there must be a corresponding debit of equal amount. For example, when a company borrows money from its bank, the company’s Cash account will enlarge and its liability account Loans Payable will raise.

It is used to assure the accounting equation Assets = Liabilities + Equity.

This system established the accounting equation where assets must always equal liabilities plus owner’s equity.

There are several transactions in a business apprehension. Each transaction, when intimately analyzed, reveals two features. One portion will be “receiving aspect” or “incoming aspect” or “expenses/loss aspect”. This is termed as the “Debit aspect”. These two aspects namely “Debit aspect” and “Credit aspect” forms the basis of the Double Entry System. The double entry system is so named since it records both the aspects of a transaction.

Features

- Assists in arranging trial balance which is an analysis of mathematical correctness in accounting.

- Preparation of closing accounts with the assist of trial balance.

- It is based upon accounting hypothesis concepts and principles.

- Each business transaction involves two accounts.

- Every transaction has two portions, i.e., debit and credit.

Example of a Double Entry System

To demonstrate double entry, let’s imagine that a business party borrows $ 2000 from a financial institute. The business party’s Cash account must be improved by $2000 and a liability account must be enlarged by $2000. To broaden an asset, a debit entrance is requisite. To raise a liability, a credit entrance is requisite. Hence, the account Cash will be debited for $2000 and the liability Loans Payable will be credited for $2000.

Characteristics of Double Entry System

The double entry system is a systematic, self-regulating and dependable system of accounting. Characteristics are stated below:

- Two parties: Every transaction involves two parties – debit and credit. Every debit of some amount creates equivalent credit or each credit creates the equivalent debit for a similar amount.

- Giver and receiver: Every transaction has to have one giver and one receiver. The amount of cash of a transaction the party gives is equivalent to the amount the party receives.

- Dual aspects: Every transaction is separated into two aspects. The left side of the business debt and the right side is credit.

- Results: Under double entry system totality of debt is equivalent to the sum of credit.

- Complete accounting system: It is a systematic and comprehensive accounting system.

Advantages:

The double entry system is approved as the best technique of accounting in the current world. Following are the main advantages of the double entry system:

- Complete accounts of transactions

Since both the aspects of a transaction are recorded, for each debit there must be a corresponding credit of an equal amount. For this reason, this system maintains accounts of all parties relating transactions.

- Verification of arithmetical accuracy

Under this method mistakes and deflections can be detected – this exerts an ethical force on the accountant and his staff. It can be detected through trial balance whether two sides of accounts are equal or not and thereby the arithmetical accuracy of the account is verified.

- Determining profit or loss

Under this method, profit and loss account can be arranged simply by taking collectively all the accounts involving income or revenue and expenses or losses and thereby the result of the business can be ascertained.

- Determining the financial position

Under this method, essential information is simply obtainable so that the organization can take a suitable assessment and run the business professionally.

- Knowing asset and liabilities

The total amount owed by debtors and the total amount owed to creditors can be ascertained easily.

- Expenditure control

Through comparative analysis, the expenditure may be controlled by curtailing expensive expenditure.

Disadvantages:

Despite so many advantages of the system, the double entry system has some disadvantages which are as follows:

- Expensive, time and labor consuming

It involves time, labor and money. So it is not possible for small concerns to keep accounts under this system. Therefore, it becomes impossible to follow this system by small business concerns.

- Persons of specialized knowledge required

An inexperienced person in accounting fails and faces problems in maintaining accounts under this double entry system

- The limited scope of application:

In a small business organization, the application of single entry system of accounting is more accepted and advantageous than double entry system.

- The problem in maintaining secrecy:

A lot of people are engaged in maintaining accounts under the double entry system since the accounting procedure is very wide and widespread.

It is clear from the above argument that the advantages of the double entry system far compensate for its disadvantages. So, it is regarded as the best system in the modern world.