Double Column Cash Book

The Cash Book having two Amount Columns on both sides is called ‘Double Column Cash Book’. The most general double column cash books are

- Cash book with discount and cash columns

- Cash book with cash and bank columns.

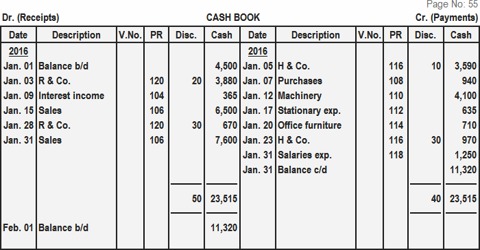

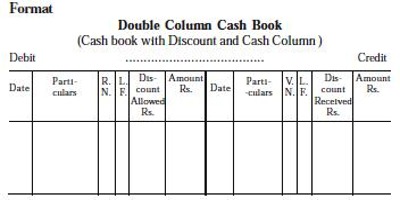

Cash Book with discount and cash columns

On either side of the single column cash book, another column is added to record discount allowed and discount received. The format is given below.

It should be noted that in the double column cash book, cash column is balanced like any other ledger account. But the discount column on each side is simply totaled. The sum of the discount column on the debit side shows the sum discount allowed to customers and is debited to Discount Allowed Account. The total of the discount column on the credit side shows total discount received and is credited to Discount Received Account.

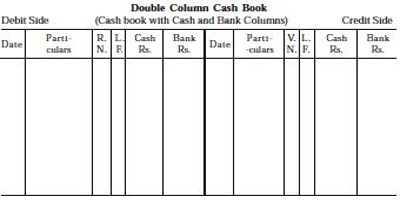

Cash Book with Cash and Bank Columns

When bank transactions are more in number, it is advisable to open a cash book by providing a separate column on either side of the cash book to record the bank transactions therein. In such case, it is not essential to open a divide Bank Account in the Ledger because the two columns in the cash book provide the reason of Cash Account and Bank Account correspondingly. It is a mixture of Cash Account and Bank Account. The format of this cash book is given below.

There are two amount columns on debit side one for cash receipts and the other for bank deposits (i.e., payment made into Bank Account). Likewise there are two amount columns on the credit side, one for payments in cash and the other for payments by cheques correspondingly.