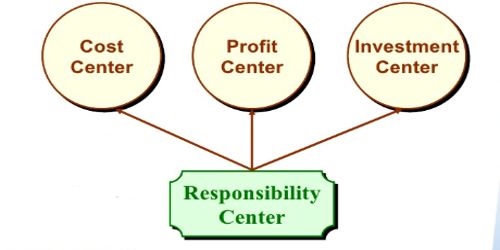

It is important to monitor the performance of cost, profit and investment centre to judge how both the centre are performing economically and how their managers are performing as managers. It is important not to judge managers for elements of performance for which they have no responsibility.

Performance measures for cost centre include:

The manager of a cost center has control over costs, but not over revenue or investment funds. Examples of cost centers include accounting, human resource, and IT departments.

Cost compared to budget: Cost centre will usually have budgets to work to so this simple comparison is very useful. However, it says nothing about what the cost centre achieved; it could spend 10% less than budget but produce only 50% of the output expected.

Cost/unit: Since a cost centre manager is responsible for costs, cost per unit produced or supplied is an obvious measure. A simple way to calculate this is to divide the costs incurred in a period by the units produced in the period.

Efficiency, capacity utilization, and production volume ratios: These relate to the use of time (and hence labor costs) in the cost centre. When setting a budget for a cost centre, it is normal to specify how long it should take to produce each item (standard hours/unit) and how many hours the factory is expected to work.