Vertical analysis (common-size analysis) is usually a popular method involving financial statement analysis that shows each item on a statement as a portion of a base figure inside the statement.

To carry out a vertical analysis of balance sheet, the total of assets plus the total of debts and stockholders’ equity are often used as base figures. All individual assets (or sets of assets if compacted form balance page is used) are shown to be a percentage of full assets. The latest liabilities, long term debts and equities are shown to be a percentage of the complete liabilities and stockholders money.

To conduct some sort of vertical analysis involving income statement, sales figure is often used as the camp and all other pieces of income statement including cost of product sales, gross profit, working expenses, income place a burden on, and net profits etc. are shown to be a percentage of sales.

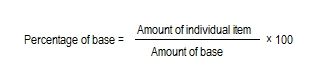

In a vertical analysis the percentage is computed by using the following formula:

A basic vertical analysis needs an individual statement for a reporting period but comparative statements may be prepared to increase the usefulness of the analysis.

Example:

An example of the vertical analysis of balance sheet and income statement is given below:

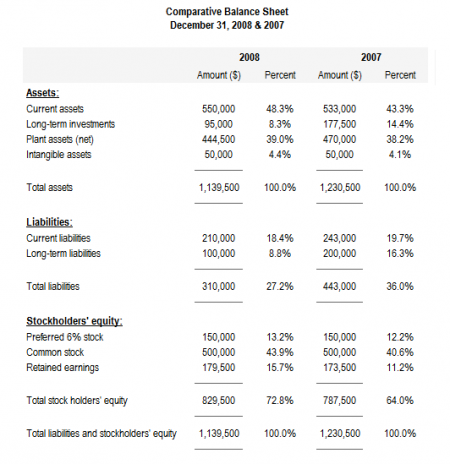

Comparative balance sheet with vertical analysis:

Current assets:

2008: (550,000 / 1,139,500) × 100 = 48.3%

2007: (530,000 / 1,230,500) × 100 = 43.3%

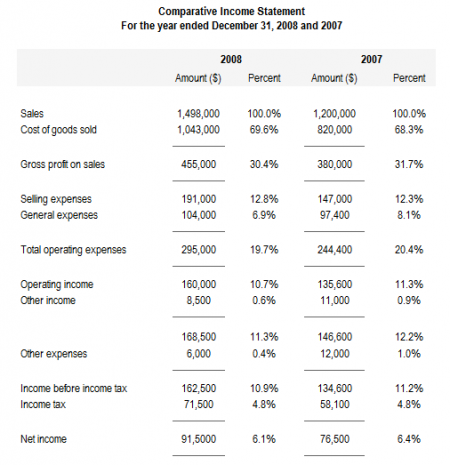

Comparative income statement with vertical analysis:

Cost of goods sold:

2008: (1,043,000/1,498,000) × 100 = 69.6%

2007: (820,000/1200,000) × 100 = 68.3%

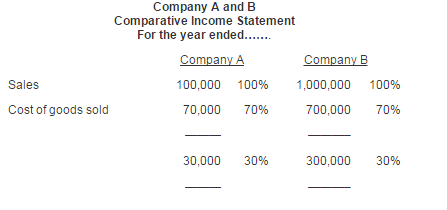

Vertical analysis states financial statements in a comparable common-size format (percentage form). One of the advantages of common-size analysis is that it can be used for inter-company comparison of enterprises with different sizes because all items are expressed as a percentage of some common number. For example, suppose company A and company B belong to same industry. A is a small company and B is a large company. Company A’s sales and gross profit are $100,000 and $30,000 respectively whereas company B’s sales and gross profit are $1,000,000 and $300,000 respectively. If vertical analysis is conducted and sales figure is used as base, it would show a gross profit percentage of 30% for both the companies as shown below: