Costs might be classified as differential, opportunity and also sunk costs. This classification is made for decision making requirements. Explanation and degrees of differential, opportunity and sunk costs get below:

Differential costs:

The work involving managers includes contrast of costs and also revenues of unique alternatives. Differential cost (also often known as incremental cost) would be the difference in price of two solutions. For example, if the cost of alternative A can be $10,000 per year and the cost of alternative B can be $8, 000 per year. The difference involving $2, 000 would be differential cost. The differential cost can be quite a fixed cost or perhaps variable cost.

In the same way the difference inside revenue of two alternatives is called differential revenue. By way of example, if alternative A’s income is $15, 000 and also alternative B’s income is $10, 000. The difference of $5, 000 could well be differential revenue.

As soon as different revenue producing alternatives are in contrast, the differential cost along with differential revenues connected with each alternative is considered.

The terms “differential cost” and also “differential revenue” utilized in managerial accounting act like the terms “marginal cost” and also “marginal revenue” utilized in economics.

Example – computation of differential cost, differential revenues and differential net operating income:

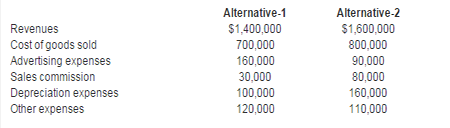

The management of Galaxy company is considering two alternatives. The costs and revenues of two alternatives is given below:

Required: Compute differential revenue, cost and net operating income from the above information.

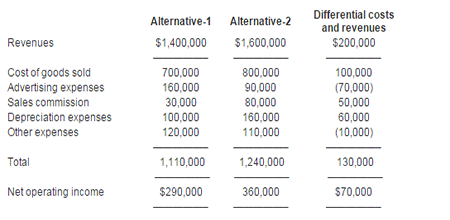

Solution

In the above example, total differential revenue is $200,000 (1,600,000 – 1,400,000), differential cost is $130,000 (1,240,000 – 1,110,000) and differential net operating income is $70,000 ($360,000 – $290,000).

If a decision is made on the basis of above computations, alternative 2 would be selected because it promises to generate more net operating income.

Opportunity costs:

Unlike other forms of cost, opportunity cost will not require the check of cash or its equivalent. It is a potential benefit or income which is given up due to selecting an option over another. One example is, You have a position in a company that pays people $25, 000 per year. For a superior future, you have to get a Master’s degree but cannot continue your job while studying. If you decide to give up your job and return for you to school to acquire a Master’s degree, you would not receive $25, 000.

Your opportunity cost can be $25, 000. Almost every alternative has an opportunity cost. It is not entered in the accounting records but must be considered while making decisions.

Sunk costs:

The costs that have already been incurred and can not be changed by any decision are generally known as sunk costs. One example is, a company purchased a machine several years ago. Due to change in fashion in several years, the products that is generated by the machine can not be sold to clients. Therefore the machine has become useless or obsolete. The price originally paid to order the machine can not be recovered by any action and it is therefore a sunk cost.