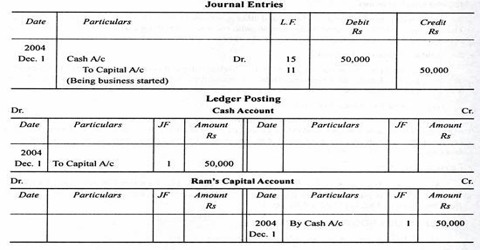

Posting Ledger

The process of transferring the entries recorded in the journal or subsidiary books to the respective accounts opened in the ledger is called Posting. Posting refers to the process of transferring entries in the journal into the accounts in the ledger. Posting to the ledger is the classifying phase of accounting.

In other words, posting means grouping of all the transactions relating to a particular account at one place. It is necessary to post all the journal entries into various accounts in the ledger because posting helps us to know the net effect of various transactions during a given period on a particular account.

For the purpose of posting, we can divide a journal entry into two parts – a debit part and a credit part. Both the parts essentially contain one or more accounts. The amount of the account (or accounts) in the debit part of the entry is written on the debit side of the respective account and the amount of the account (or accounts) in the credit part of the entry is written on the credit side of the respective account in the ledger.