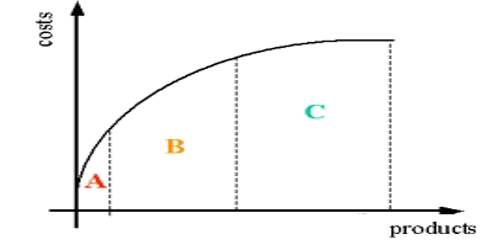

ABC Analysis

In materials management, the ABC analysis (or Selective Inventory Control) is an inventory categorization technique. ABC analysis divides an inventory into three categories – “A items” with very tight control and accurate records, “B items” with less tightly controlled and good records, and “C items” with the simplest controls possible and minimal records. The ABC analysis provides’ a mechanism for identifying items that will have a significant impact on overall inventory cost, while also providing a mechanism for identifying different categories of stock that will require different management and controls.

Activity Based Costing, or ABC, is a method of allocating overhead and direct expenses related to the most important activities of the company first. This process allows business owners and managers an opportunity to better define the areas of manufacturing or sales that generate the most profit for the company. Inventory analyzed under the ABC method is classified in order of profitability to the company. Class A inventory accounts for 80 percent of revenue, class B inventory for 15 percent of revenue and class C inventory for 5 percent of revenue.

(a) Better Control of High-Priority Inventory

ABC inventory analysis places tighter and more frequent controls on high-priority inventory. High-priority inventory, or class A inventory, is the class of inventory that customers request most often. In manufacturing, class A inventory also can include the items most often used in the production of goods. Because Class A inventory is directly linked to the success of the company, it is important to constantly monitor the demand for it and ensure stock levels match that demand. With ABC analysis, your company can use its resources to prioritize control of high-priority inventory over inventory that has a lower impact on your bottom line.

(b) More Efficient Cycle Counts

Under the ABC inventory analysis method; you can allocate your resources more efficiently during cycle counts. A cycle count is a process of counting only certain items on schedule dates. The frequency of your cycle counts and the items you choose to include depends on how often your inventory fluctuates. Once inventory is organized by class, you can focus regular cycle counts on class A inventory. Depending on your needs, it may be necessary to count class B inventory as infrequently as twice per year and class C inventory only once per year. The ABC analysis method saves time and labor counting only the inventory required by the cycle for the class of inventory versus counting all inventory items each cycle.

(c) Conflict with Other Cost Systems

The ABC inventory analysis does not meet Generally Accepted Accounting Principles (GAAP) requirements and also conflicts with traditional costing systems. Companies that use ABC methods must operate two costing systems, one for internal use under the ABC method and -another for compliance with GAAP. Traditional costing systems generate the figures required GAAP. Traditional costing systems allocate cost-drivels-by the actual unit cost, rather than by the activity percentage of the cost driver. As a result, ABC cost assignments often differ from traditional cost system assignments.

(d) Requires Substantial Resources

The ABC method requires more resources to .maintain than traditional costing systems. When cycle counts are performed, class A inventory must be routinely analyzed to determine if the inventory still consists of high-priority items. If an inventory piece is no longer used or demanded as frequently, it is moved to another inventory classification. This constant process requires much more data measurement and collection.