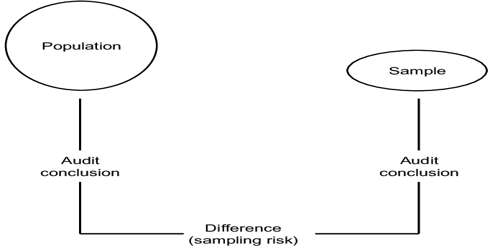

Sampling Risk refers to the possibility that the sample drawn is not representative of the population and that, as a result, the auditor will reach an incorrect conclusion about the account balance or class of transactions based on the sample. It is the possibility that the items selected in a sample are not truly representative of the population being tested. This is a major issue since an auditor does not have the time to examine an entire population and so must rely upon a sample. It helps auditor to have the principle to make a conclusion on the total population.

Sampling risk represents the possibility that an auditor’s conclusion based on a sample is different from that reached if the entire population were subject to audit procedure. The auditor may conclude that material misstatements exist, when in fact they do not; or material misstatements do not exist but in fact, they do exist. Auditors can lower the sampling risk by increasing the sampling size. Sampling risk is one of the many types of risks an auditor may face when performing the necessary procedure of audit sampling. Audit sampling exists because of the impractical and costly effects of examining all of a client’s records or books. The effectiveness and the efficiency lie on the auditor who can reduce the sampling risk by picking up a sample that is truly representative of the p0pulation. A carefully selected sample will decrease the rate of sampling risk.