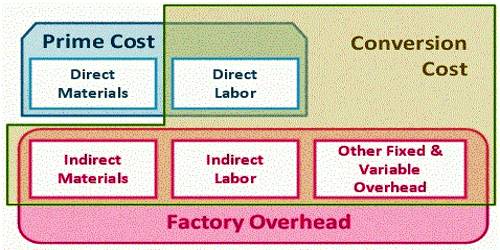

Conversion Cost

Conversion costs are those costs required to convert raw materials into finished goods that are ready for sale. They are the combination of direct labor costs plus manufacturing overhead costs. The concept is used in cost accounting to derive the value of ending inventory, which is then reported in the financial statements. It is the amount incurred during the transformation of raw materials inventory into finished goods. If can also be used to determine the incremental cost of creating a product, which could be useful for price setting purposes. Since conversion activities involve labor and manufacturing overhead, the calculation of conversion costs is:

Conversion costs = Direct labor + Manufacturing overhead.

Thus; conversion costs are all manufacturing costs except for the cost of raw materials. If you add direct labor costs and manufacturing costs, the sum that you get will be the conversion cost. Examples of costs that may be considered conversion Costs are:

a) Direct labor and related benefits,

b) Equipment depreciation,

c) Equipment maintenance,

d) Factory rent,

e) Factory supplies,

f) Machining,

g) Production utilities

As can be seen from the list, the bulk of all conversion costs are likely to be in the manufacturing overhead classification. They are the costs incurred to convert raw materials into finished products.